NYSLRS pension payment options are designed to fit your needs after you retire. Understanding these options will make it easier for you to choose the one that’s right for you.

While the basic option, the Single Life Allowance, would provide you with a monthly payment for the rest of your life, all payments would end at your death. Other options, in exchange for a reduced benefit, allow you to provide for a spouse or other loved one after you’re gone.

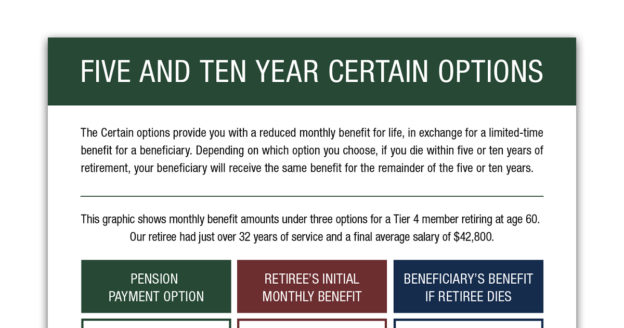

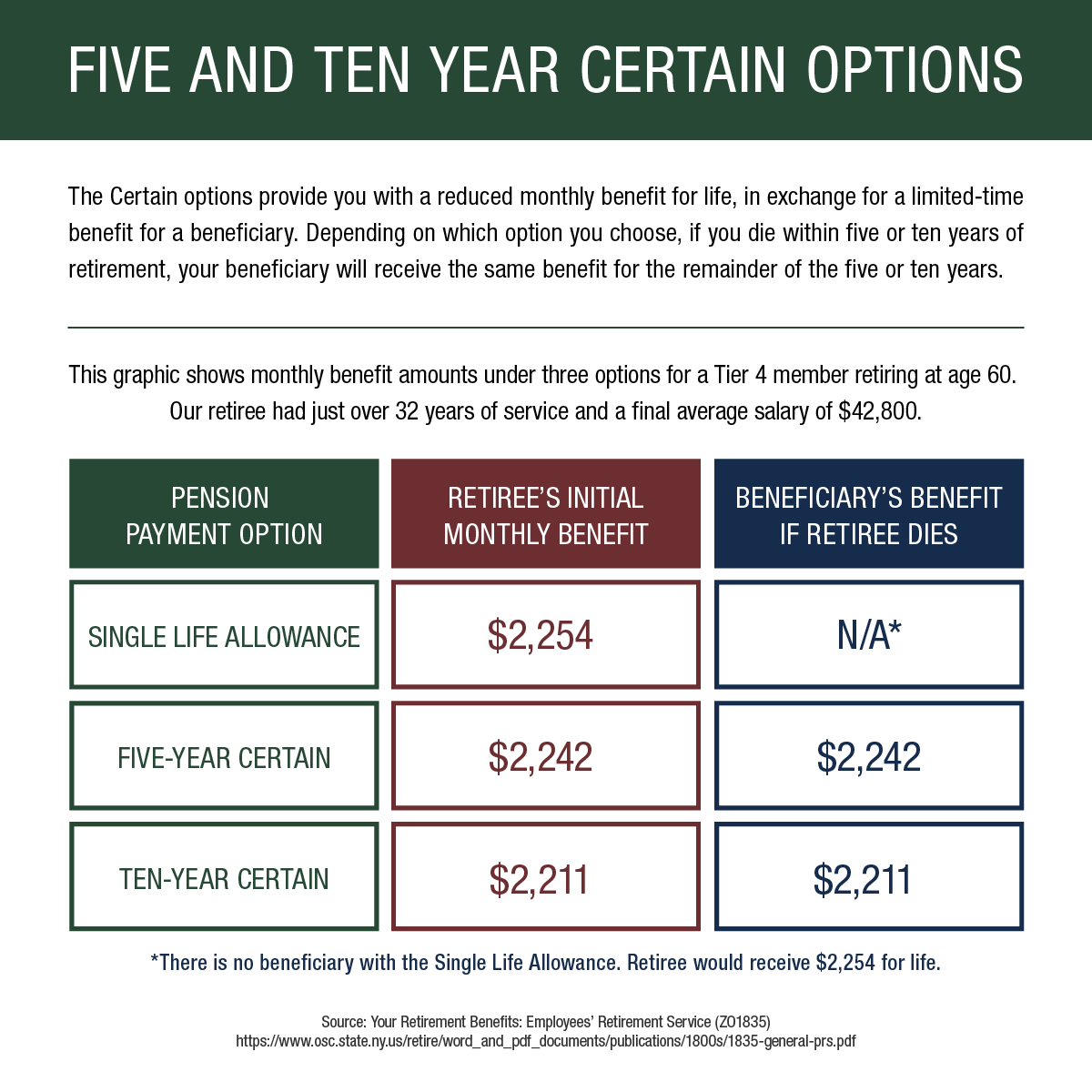

Five and Ten Year Certain options don’t provide a lifetime benefit for a beneficiary, but they have advantages you may want to consider.

How These Pension Payment Options Work

The Five Year Certain or Ten Year Certain options provide you with a reduced monthly benefit for your lifetime. If you die within the five- or ten-year period after your retirement, your beneficiary would receive pension payments for the remainder of the five or ten years. If you live beyond the five- or ten-year period, your beneficiary would not receive a pension benefit upon your death.

Let’s say you choose the Five Year option. If you die two years after retiring, your beneficiary will receive a benefit for three years. If you choose the Ten Year option, and die after two years, your beneficiary will get a benefit for eight years. In either case, your beneficiary would receive the same amount you were receiving, though they would not be eligible for any COLA increases.

Another feature of these plans is that you can change the beneficiary at any time within the five- or ten-year period.

Whatever your situation, you should review the payment options and choose carefully. Visit our Payment Option Descriptions page for details about all available pension payment options. For a better idea of how these payment options would work out for you and your beneficiary, try our online Benefit Calculator.

If you pass away after retiring for 3 or more years do you get 10% of the death benefit you would have gotten at age 60 plus what you paid in or just the 10%?

For a NYSLRS retiree who is eligible for a post-retirement death benefit, after the second year of retirement, the value of the benefit would be 10% of the benefit payable at retirement (or at age 60, if that is earlier). A beneficiary would not receive the retiree’s accumulated contributions to NYSLRS.

You can find more information on our Death Benefits – Retirees page.

In June 2019 I went into the loan office , I applied for the balance in my account due to me having an outstanding loan balance, and leaving the county for a new job elsewhere I was told it would be 10 weeks when I will receive the balance in my account. Today I follow-up and was told my application was receive 8/2/2019 and it will be 10 weeks from 8/2/2019. How can that be.? Just asking

We apologize for the delay. To get the account-specific information you need, please email our customer service representatives using the secure form on our website (http://www.emailNYSLRS.com). One of our representatives will review your account and respond to your questions. Filling out the secure form allows us to safely contact you about your personal account information.

I see on the website that Alternative payment options are available when collecting a pension. Is a one time lump sum payment option available?

Alternative Options

If the options described here do not meet your needs, we will consider written requests for other payment methods. These requests must be outlined in detail by you and then approved by us for legal and actuarial soundness.

To get the account-specific information you need, please email our customer service representatives using the secure email form on our website. One of them will review your account and respond to your questions. Filling out the secure form allows us to safely contact you about your personal account information.

I was told they raised the $30,000 earning cap but I can’t find that confirmation. Does anyone know if that’s true ?

Under current State law, NYSLRS retirees can earn up to $30,000 per calendar year from public employment without a reduction in their pension. There is generally no earnings limit once the retiree is 65.

Both houses of the Legislature have approved a bill that would increase the earnings cap to $35,000 starting in 2020. However, the bill must be signed by the Governor to become law. To our knowledge, the Governor has not signed this legislation.

Hello, Does this state law apply to Florida state also?

The $30,000 earnings limit for NYSLRS retirees applies to retirees who are working for a public employer in the State of New York. If you have additional questions about working after retirement, please read our publication, Life Changes: What If I Work After Retirement?