Here is an important retirement planning tip — most members can create their own pension estimate in minutes using Retirement Online. Your estimate will be based on the most up-to-date account information we have on file for you. You can enter different retirement dates to see how those choices would affect your benefit. When you’re done, you can print your pension estimate or save it for future reference.

How to Create a Pension Estimate

To get started:

- Sign in to Retirement Online.

- Click the ‘Estimate my Pension Benefit’ button to access the pension calculator.

- Enter the date (or age) you plan to retire.

You can fine tune your estimate by entering your annual earnings and expected pay increases. You can also include any service credit you plan to purchase. If you add the birthdate for a beneficiary, you’ll see the estimated monthly payment amounts under the pension payment options that provide a benefit for a survivor.

Remember, the pension amounts you’ll see are just an estimate; it is not a guarantee of what you’ll receive when you retire.

Most Tier 2 through 6 members (more than 90 percent of all NYSLRS members) can use the Retirement Online pension calculator. However, some members may not be able to because of their circumstances — for example, members who recently transferred to NYSLRS, some PFRS members, or Tier 6 members with between five and ten years of service. The system will notify you if your estimate cannot be completed using the Retirement Online pension calculator. Please contact us to request a pension estimate if you receive this notification.

Do More With Retirement Online

In Retirement Online, you can view your date of membership, tier, retirement plan, estimated total service credit and more. Purchase previous service credit well before retirement and save on interest costs. Check out what else members can do in Retirement Online.

If you don’t already have an account, learn more and register for one today. If you need help with Retirement Online, read our Retirement Online Tools and Tips blog post.

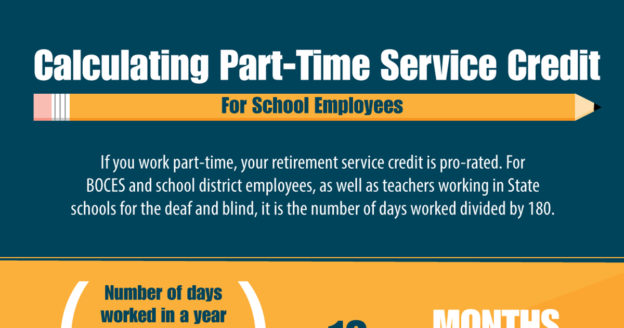

While most New York teachers and administrators are in the

While most New York teachers and administrators are in the

{kind=link}