If you have tax-deferred retirement savings (such as certain 457(b) plans offered by NYS Deferred Comp), you will eventually have to start withdrawing that money. After you turn 70½, you’ll be subject to a federal law requiring that you withdraw a certain amount from your account each year. If you don’t make the required withdrawals, called Required Minimum Distributions (RMDs), you could face significant penalties.

If you have tax-deferred retirement savings (such as certain 457(b) plans offered by NYS Deferred Comp), you will eventually have to start withdrawing that money. After you turn 70½, you’ll be subject to a federal law requiring that you withdraw a certain amount from your account each year. If you don’t make the required withdrawals, called Required Minimum Distributions (RMDs), you could face significant penalties.

RMDs are never eligible for rollover into other retirement accounts. You must take out the money and pay the taxes.

Calculating the Distribution

The RMD amount must be calculated annually. It’s based on the account’s balance at the end of the previous calendar year and the life expectancy of you and your beneficiary. Check out AARP’s Required Minimum Distribution Calculator for an easy way to determine your required distributions. Many retirement plan administrators, including the New York State Deferred Compensation Plan, will inform you of your RMD amount, but it’s your responsibility to take the required distribution.

Potential Penalty

If you don’t take the required distribution, or if you withdraw less than the required amount, you may have to pay a 50 percent tax on the amount that was not distributed. (You must report the undistributed amount on your federal tax return and file IRS Form 5329.)

The IRS may waive the penalty if you can show that your failure was due to a “reasonable error” or that you have taken steps to correct the situation. You can find information about requesting a waiver on page 8 of the Form 5329 instructions.

What Accounts Require Minimum Distributions?

Most retirement accounts you’re familiar with require these annual withdrawals:

- 457(b) plans

- IRAs (traditional, SEP and SIMPLE)

- 401(k) plans

- 403(b) plans

- Profit-sharing plans

- Money purchase plans

Since contributions to Roth IRAs have already been taxed, the IRS does not require distributions from Roth IRAs at any age.

As with most things investment-related, a lot depends on your particular circumstances. If you have questions, contact your financial advisor or your plan administrator.

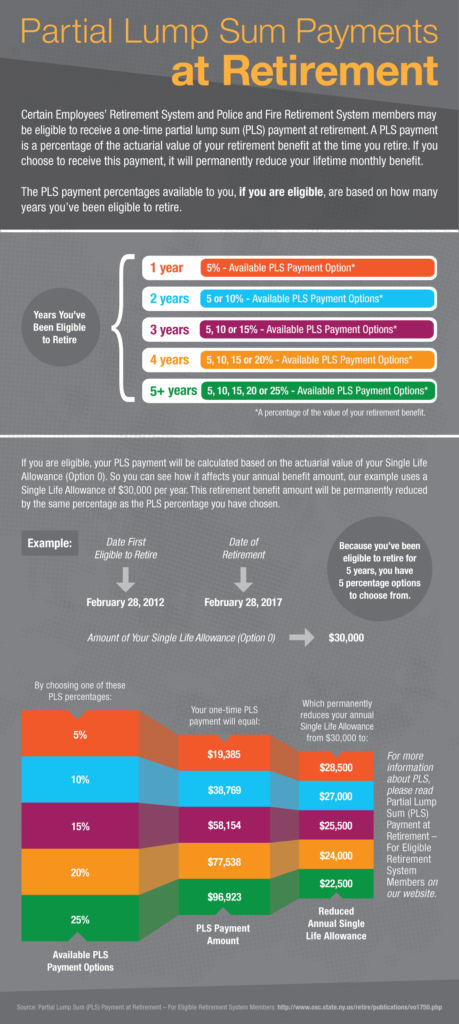

How the Partial Lump Sum Payment Works

How the Partial Lump Sum Payment Works